Time to Party Like its 1999

All systems go for a blow-off top; let's make hay while the sun's shining.

The melt-up is on.

Last week, I made the case for an imminent blow-off top in U.S. equities. At the time, the large-cap Nasdaq and S&P 500 indices had already cleared new record highs… but small caps were stubbornly sitting on the sidelines.

That changed late last week, when the Russell 2000 staged a massive breakout from a 9-month consolidation pattern, confirming a broad-based rally across risk assets:

There’s no other interpretation: this is some of the most bullish price action you’ll see. Instead of chalking the rally up to “irrational mania”, let me set aside my bearish bias and give the bulls their due.

If we analyze the rearview fundamentals, things have never looked better for corporate America. The chart below shows U.S. profit margins reaching new record highs in the wake of the latest Q3 earnings reports:

But don’t worry, I haven’t gone full bull. There’s one glaring problem you might notice in the chart above, as the great Jeremy Grantham once noted:

“Profit margins are the most mean-reverting series in finance.”

Different This Time? Don’t Bet On It

History shows that profit margins ALWAYS look best just before they fall off a cliff. That means stocks only appear reasonably priced today if you assume a “permanently higher plateau” of the highest profit margins in history. Sure, it could be “different this time”… but that’s not a bet I’m willing to make.

After all, the U.S. government just pumped $5 trillion into the economy in 18 months. Is anyone surprised that corporations enjoyed a temporary windfall of profitability? Does anyone really expect a repeat performance from here?

Despite the recent passage of the much-touted $1.2 trillion infrastructure package over the weekend, that’s not nearly enough to offset the broader fiscal and monetary drag going into 2022 and beyond. Barring another unprecedented economic crisis, the U.S. economy is entering stimulus withdrawal mode from here on out.

Thus, my working assumption is that today’s record profit margins will eventually mean-revert when the business cycle turns. I’ve previously written about how this will likely happen - spiking inflation and monetary tightening today, giving way to deflation and slower growth tomorrow.

Now, here’s where I get to put my bear cap back on…

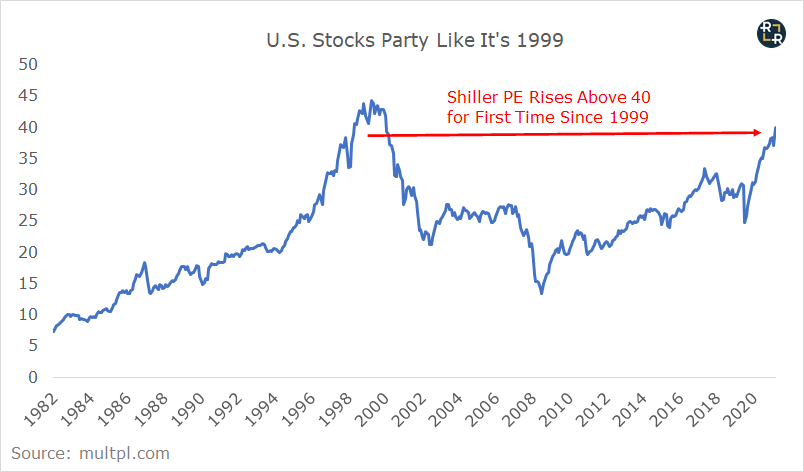

The Shiller PE Ratio provides a useful valuation metric for normalizing earnings over a 10-year period. This smooths out cyclical swings in profit margins, and helps paint a picture for the long-term valuation of the market. And it’s not just an academic metric - the Shiller PE ratio provides one of the most reliable predictors of long-term returns (i.e. high ratios correspond with lower future returns, and vice versa).

The punchline: last week, the Shiller PE ratio for the S&P 500 rose above 40 for the first time since January 1999:

In the long run, this is almost as bearish as it gets. But that’s a problem for another day.

For now, investors are myopically focused on what they can see in the here and now. Instead of pricing in the inevitable mean reversion in corporate profit margins, investors have instead extrapolated a one-time windfall into perpetuity.

We already have a preview for what happens when this mirage fades.

The Death of the “Disruptors”

The “Disruptive Innovation” cohort has become littered with the corpses of busted narratives. Countless story stocks enjoyed incredible valuation inflations, driven by the temporary windfall of pandemic profits.

Peloton is the case study du jour. We all know the story here - pandemic lockdowns created a temporary windfall in demand for at-home fitness products. Investors extrapolated a short-term fitness fad into an enterprise value exceeding $50 billion at its peak. Wall Street analysts were happy to supply the market with fantastical projections of endless TAM (total addressable market) growth, multiple new product offerings, and “software as a service” margins.

In the last few months, visions of grandeur have collided with cold, hard reality: it’s an overpriced stationary bike mounted with an iPad. Like every other hit fitness product of the last 50 years, Peloton bikes across the country are rapidly turning into $1,500 clothes hangers, as consumers grow bored and move on to the next fitness fad.

Shares collapsed 30% overnight after the company missed Wall Street’s lofty revenue and earnings expectations across the board last week. The stocks is now down 70% from its highs. It’s but one of countless examples of busted story stocks, where visions of grandeur and endless TAMs have given way to the harsh reality of competition and margin compression.

These fallen angels in the “Disruptor” space shows that, despite how great the near term prospects, overpaying today for the promises of tomorrow rarely pans out for long-term investors.

This is a small preview of the same fate awaiting the broader markets when the reality of temporary stimulus-induced growth fades in 2022 and beyond. We’ve got a long way to go from here to correct the excesses of today’s mania. That’s not just my opinion - legendary investor Stan Druckenmiller laid it out last Thursday at the Boston Investment Conference:

But if there’s one lesson we can take away from today’s market, it’s that momentum and narratives can defy financial gravity in the short run. With a solid Q3 earnings season nearly under wraps, plus the passage of new infrastructure stimulus, investors have every reason to bid stocks higher in the short run.

Given the broad-based breakouts to new all-time highs in all major U.S. indices, there’s money to be made by leaving bias at the door and playing the cards Mr. Market has dealt. As mentioned last week, late stage melt-ups - like the one I believe is just getting started - can produce stunning gains in very short periods of time.

So let’s try to make some hay while the sun is shining. In the next section, I’ll detail a basic options trade that could produce better than 500% returns in the event of a continued melt-up into year end.