The Holy Grail of Investing

How to achieve compounding nirvana

For most investors, earning higher returns means picking better stocks. For others, it means taking more risk.

But what if there was another way? A far easier path for unlocking higher returns, while also reducing the risk in your portfolio?

Turns out, this approach does exist - the proverbial “Holy Grail” of investing.

Those aren’t my words. That’s how billionaire investor Ray Dalio - founder of the world’s largest and most profitable hedge fund - once described the investment principles I’ll share with you today.

There’s no real secret here. We’re simply dealing in the mathematics of wealth compounding. Professional money managers have exploited this science for decades to generate outperformance. As you’ll see today, the concepts are fairly straight-forward. The real challenge? Maintaining the discipline and conviction required to translate theory into practice.

I was lucky. Starting out in the financial world, I worked with a CIO and mentor who built an entire investment strategy around these principles. For three years, I saw firsthand how he applied theory into real-world investing, with hundred-million-dollar table stakes.

This Holy Grail approach goes beyond the world of stock picking. These principles work uniformly across any game of wealth compounding - poker, blackjack, sports betting, insurance underwriting - you name it.

Today, I’ll showcase the Holy Grail strategy using a basic coin flipping game.

A Coin Flipping Proposition

Imagine I offered you the following betting proposition...

We’ll flip an honest coin 10 times, and you’ll earn 100% on heads versus a 50% loss on tails. Plus, I’ll guarantee you a final outcome of 5 heads and 5 tails.

Let’s assume you’ve got $100 to play with, and that you’re a rational investor seeking to maximize your returns.

Assuming you like money, you should jump at the opportunity.

After all, this bet guarantees you a 25% average return, or $25 per coin flip. That’s based on the following expected value formula:

Expected value = (win probability x amount won) - (loss probability x amount lost)

Coin flipping expected value = (0.5 x $100) – (0.5 x $50) = +$25 per coin flip

So, the only question left is… how much of your $100 do you put at stake to maximize your returns?

Ask 100 people this question, and 99 will say bet the full $100 (myself included when first presented with this question). After all, if you can expect an average 25% return, you’ll make the most money by betting as much as possible, right?

Not so fast.

It turns out, the max betting option leaves quite a bit of money on the table.

Here’s why…

Betting the Maximum, Earning the Minimum

Let’s run through the math of betting the full $100 on the 10 coin flips.

But first, a quick note: the order of returns here is immaterial. You’ll arrive at the same end result regardless of whether you flip five heads followed by five tails, or alternate evenly between heads and tails, or combination in between.

In these examples, the coin will alternative evenly between heads and tails.

With that said, let’s see what happens when you put your full $100 “Portfolio” to work across the 10 coin flips in the “Max Bet” strategy:

Not a great result: you end up precisely where you started, with $100 in your pocket.

So, despite earning a 25% average return, your compounded return was 0%.

What happened here?

The answer lies in the highlighted cells above - the extreme volatility eroded your compounded returns down to zero. This phenomenon is known as the “volatility tax” - the silent thief robbing your portfolio of its full compounding potential.

Volatility: The Hidden Tax in Your Portfolio

You can think of volatility as a sort of drag coefficient on your portfolio - it determines how efficiently you transform potential (i.e. average) returns into realized (i.e. compounded) returns.

The mathematical relationship at work here is expressed as follows:

Which can be rearranged as:

In plain English, the math says you have two options for boosting your bottom line as an investor:

1) Increase your average returns, or

2) Reduce your volatility.

Most investors spend 99% of their time focusing on option number one. After all, that’s the sexy part, right? Everyone wants to find the next hot stock that can double or triple in value.

But in many cases, the far easier path for boosting your compounding efficiency comes from simply reducing the volatility tax incurred in your portfolio.

We can see how this works by revisiting our coin flipping example…

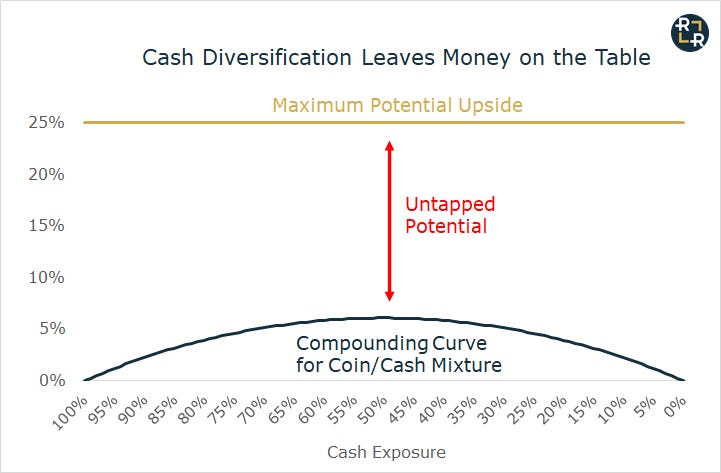

Lowering Your Volatility Tax

Let’s re-run the same betting sequence as before, but with one twist: cut your bet size down. Instead of putting 100% of your money at risk, keep half of your portfolio sitting in cash on the sidelines. In order to maintain this constant 50% exposure, rebalance your portfolio before each coin flip.

Here’s how the math works out in this “Half Bet” scenario:

Voila! The simple act of cutting your bet size in half boosts your final cash pile from $100 to $180.

Notice in the bottom of the table, you simply cut your average returns and volatility in half. But because of the non-linearity at work, this had a greater than 1-for-1 impact on your compounded returns, which grew from zero to 6.1%.

The non-linear relationship at work here is shown below, where a 50% bet size optimizes your coin flipping returns:

(Note: for any given risk/reward proposition with fixed odds, the “Kelly Criterion” formula will pinpoint the exact bet size for optimizing your compounded returns).

Another way of framing the situation is that you used cash as a diversifying agent. The cash provided you with a non-correlated return stream. That’s precisely what Ray Dalio refers to as the “Holy Grail of Investing”, which he summarizes as follows:

“With fifteen to twenty good, uncorrelated return streams, you can dramatically reduce your risks without reducing your expected returns.”

Now, you may have picked up on a major shortfall in our approach so far - the zero returns available from holding cash. After all, we have a coin flipping scheme capable of generating 25% average returns… and yet, we max out at 6.1% compounded returns when using cash as a diversifier:

Fortunately, we’ve got one final trick up our sleeve to harvest this untapped potential…

Negative Correlation and Compounding Nirvana

Let’s re-run the coin flipping proposition, except this time, we’ll add an “Inverse Coin” into the mix.

As the name implies, the Inverse Coin produces the exact opposite outcome of the Regular Coin (i.e. 50% loss on heads versus a 100% gain on tails). In mathematical terms, these two coins enjoy a perfect negative correlation with one another.

The table below shows the result of maintaining a constant 50/50 exposure to these negatively correlated coins:

Welcome to compounding nirvana – the perfectly efficient transformation of average return potential into compounded wealth, through total volatility reduction.

Note how, despite each individual coin incurring substantial volatility, the 50/50 portfolio never incurred a single loss – perfectly compounding at 25% across all 10 trials.

That’s the power of perfectly negative correlation. Each time one coin loses money, the other delivers offsetting profits, suppressing volatility down to zero.

We can see this process at work in the chart below, with each coin’s volatile path plotted against the perfectly smooth portfolio value:

Sadly, you most likely won’t find such a perfect combination of assets in the real world (but please call me if you do). The exercise showcases the ideal scenario, so that you know what to aim for, within the constraints of reality.

In most cases, you’ll do well if you can find high performing assets with low or zero correlation. And when you can identify high performing return streams with negative correlation, you get that much closer to compounding nirvana.

As it turns out, these opportunities are not as rare as you might think.

Putting Theory into Practice

In some cases, the market environment itself presents an opportunity to combine asset classes or individual stocks that enjoy low or negative correlations. As one example, in today’s market, the S&P 500 and Nasdaq have increasingly become the same “long duration” bet that rises and falls with long-dated Treasuries.

Energy stocks, on the other hand, offer a deeply negative correlation with Treasuries on a trailing 1-year basis:

Ross Report premium subscribers are taking advantage of this unique opportunity today. Subscribers get access to a live tracking portfolio that that contains high-quality individual energy stocks, hedged against broader-market risk with long exposure in Treasuries.

Subscribers get access to a “Long-Only” portfolio that has outperformed the S&P 500 and the Nasdaq since its inception. Even more impressive, that outperformance has come despite only 40% equities exposure. Click here to check it out for yourself:

In other cases, you can use more advanced strategies to engineer offsetting correlations yourself.

Ross Report subscribers get access to a basic options trading strategy, designed to generate uncorrelated or negatively-corelated returns, including…

Selling covered call options to create negatively correlated income against existing long positions.

Buying call and put options designed to generate negatively correlated hedging profits during market downturns.

I draw upon deep dive fundamental research and macro factors to select investment ideas, and then express those ideas using stocks, ETFs and options - all tracked in a “Unconstrained” portfolio. Subscribers all get access to real-time trade alerts issued during the trading day, and weekly portfolio reviews.

As a final note, there’s one key challenge that goes beyond simply understanding the principles outlined in this article. Implementing these concepts in practice often requires extreme conviction and discipline.

The Challenge of True Diversification

In the real world, you can often go months or years on end when the diversifying agents in your portfolio underperform. This is a feature, not a bug of “true diversification” - where your portfolio contains assets that move opposite one another.

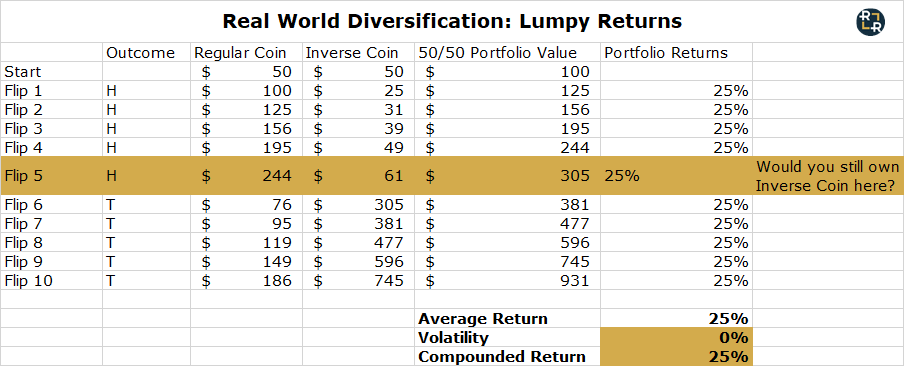

Let’s briefly revisit the coin flipping example to see what this looks like. Instead of a smooth back and forth, where each asset takes turns generating positive returns, you might see something more lumpy in practice, like five heads followed by five tails:

Here’s the million-dollar question: how many of us would maintain exposure to the “Inverse Coin” after five periods of non-stop losses in the real world?

Our natural inclination is to “fix” the thing that isn’t working. But with true diversification, the thing that appears “broken” may be performing its role exactly as intended. A portfolio filled with assets that always go up together is probably a portfolio where everything can go down together, too.

Therein lies the paradox and challenge of “Holy Grail” investing. You must be willing tolerate the pain of always having one part of your portfolio underperforming, or even losing money, without changing course.

If you’re interested in learning more about translating the theory of Holy Grail investing into practice, click the subscribe button below: