Prepare for Turbulence as the Fiscal and Monetary Cliff Approaches

Global growth is slowing even before massive stimulus withdrawal

Welcome to the first official edition of the Ross Report, and thank-you for subscribing!

As you might know, my core thesis is that we’re living through the greatest financial mania of all time. Of course, that information alone doesn’t do anyone any good. The trillion dollar question - when does it all unravel?

I won’t pretend to offer any insights into short-term market moves. But if you look out over the next 12 months, all signs point towards a shift from economic boom to bust.

Today, I’ll outline the key monetary and fiscal forces that will catalyze this turn in the market cycle. Plus, I’ll detail the current evidence of a coordinated global slowdown, even before these headwinds gather strength in the months ahead.

Let’s get started…

Get Ready for a November Taper

Financial markets have just enjoyed one of the greatest short-term sugar rushes of all time, thanks to the record monetary stimulus of the last 18 months. Unfortunately, the hangover is quickly approaching.

That’s because all signs point towards an imminent withdrawal of central bank stimulus. One of the key mouthpieces for U.S. Federal Reserve (Fed) policy - the Wall Street Journal - released this headline Friday morning:

If you’ve followed the markets for long, you know that headlines like this are no accident. Outlets like the WSJ make up part of the Fed’s unofficial “forward guidance”, designed to help prepare the markets for key shifts in policy. So I’m taking the headline at face value, and fully expecting a November taper. That means Fed officials will likely make the official announcement at the upcoming Sept 21 - 22 FOMC meeting.

Might the markets shrug this off as no big deal in the short-run? Maybe… or maybe not. I’m not here to guess the next 100 points in the S&P 500. But if you look out 12 months from now, it’s clear the Fed is preparing to shift from the loosest monetary policy ever towards outright tightening. That’s a major problem for a stock market trading at the highest valuation in history.

Meanwhile, my new favorite Fed indicator - Bob Kaplan’s brokerage account - also points at an imminent taper. After actively trading stocks, bonds and futures contracts in sizes exceeding $1M, all while the Fed supplied the largest monetary stimulus of all time, Kaplan has suddenly committed to dumping his stocks on “ethical concerns”.

Let’s please take a moment to recognize this heroic decision. Liquidating stocks at all-time highs, just before the punch bowl gets taken away. Well done, sir.

Moving on, this critical shift in monetary policy isn’t isolated to just the U.S.

Monetary Tightening Goes Global

Central banks around the world are currently on track to shift from monetary expansion to contraction by Q4 of next year:

On the surface, this degree of “tightening” may seem laughably miniscule. But there’s a reason why monetary stimulus is often compared to taking drugs - markets build up a stimulus tolerance over time. So once you go down the easy money path, even the slightest reversal creates one helluva hangover.

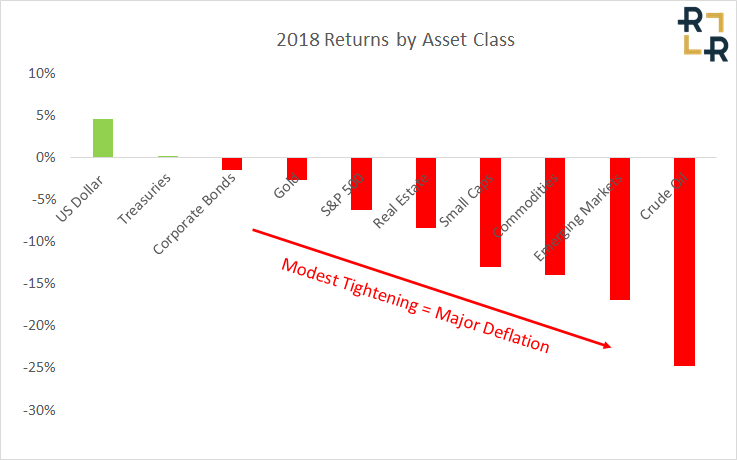

Need proof? Simply rewind the clock back to the only semi-serious tightening effort of the last decade - 2018. The Fed hiked rates a measly 100 basis points, and trimmed its balance sheet from $4.4 trillion to $4.1 trillion, before this happened:

The only difference between now and 2018 is that the economy and financial markets have become even more hopelessly addicted to monetary and fiscal stimulus. And therein lies the second key macro risk looming on the horizon - the upcoming fiscal cliff.

Goodbye Stimulus, Hello Fiscal Cliff

It’s hard to overstate the importance of fiscal support underlying today’s economy. The easiest way to paint the picture is to simply rewind the clock back to March 2020, when markets were in free-fall. It wasn’t the central banks that saved us. Recall that on Sunday March 15th, 2020 the New York Fed announced a $700 billion quantitative easing package, and slashed interest rates to zero. The next day, U.S. stocks suffered their single largest daily decline since the 1987 Crash.

The markets didn’t stabilize until the March 19th announcement of a $1 trillion stimulus package, including direct payments to households. Mr. Market quickly figured out that these direct transfer payments would create a windfall for economic growth and corporate profits, which is exactly what we got. But now, there’s one big problem…

The stimulus checks are no longer flowing.

Plus, the historic federal unemployment supplements launched in the wake of COVID-19 officially ended last week. The unwind of these and other stimulus programs means that Federal budget deficit will collapse by 60% next year, sending the U.S. economy over one of the largest fiscal cliffs ever:

In the long run, shrinking government deficits are a great thing. Resources are more efficiently managed in the private sector. But even though getting off drugs is great for your long-term health, it creates major pain in the interim. The same applies to fiscal stimulus withdrawal, which will send shockwaves throughout the economy in the short run.

Meanwhile, millions of consumers are also on the verge of losing a major short-term boost to their pocketbooks - one that doesn’t show up in the official government spending numbers - nationwide eviction moratoriums. This effective wealth transfer from landlords to consumers provided a major artificial consumption boost for millions of households over the last 18 months. But now, the bill is coming due. Millions of delinquent homeowners and renters will soon be forced to either repay their accumulated debts or face eviction.

That means less disposable income and more housing supply incoming. So not only is this a problem for short-term consumption and economic growth, it’s also a major problem for the housing market. The combination of record stimulus payments plus the artificial supply constraints created from eviction moratoriums re-inflated a brand new housing bubble in the post-COVID economy. Home prices are roughly as overvalued as they were the peak of the Real Estate Bubble in 2006:

In the short-term, this created a massive positive wealth effect. Trillions in temporary economic gains were created from a) rising home equity and b) an artificial income boost for millions of Americans not making rent/mortgage payments. Now, the stage is set for a reversal.

If you own a home, there’s almost never been a better time to sell. If you plan on buying, you might wait a few years. I’m personally holding out for a nationwide half-off liquidation sale.

Add it all up, and we’re looking at a pretty grim macro backdrop for 2022.

But it gets worse. Even before these headwinds start showing up in the coming months, cracks have already emerged in the global growth picture.

Global Growth Slowing Ahead of Fiscal/Monetary Cliffs

Starting in the U.S., third quarter economic forecasts have recently plunged. The chart below shows that the Atlanta Fed’s Q3 GDP forecast recently dropped from an estimate of 6% growth in late August to just 3.7% today:

Yes, 3.7% growth is still good - but the trajectory and magnitude of deceleration hints at trouble ahead.

Looking abroad, the situation doesn’t appear any better. In the Eurozone, the September reading of the key ZEW Economic Index took a big hit, dropping to 31.1 from a previous reading of 42.7. That also massively missed consensus expectations of a rebound back to 52.2 for the month.

But by far, the biggest global headwind is coming from China.

This topic deserves its own article, but to make a long story short, China led the world out of the 2008 Financial Crisis. There was just one problem - it took on a record amount of debt in the process. A substantial portion of that debt went into China’s real estate sector, which is now coming unglued. Real estate developer Evergande, and it’s $300 billion in liabilities, currently sit at the epicenter of distress. The company’s shares have lost 75% of their value this year, and default seems imminent.

But this one company only forms the tip of the iceberg. The pressure is rippling throughout China’s corporate bond market. The chart below shows how high-yield corporate bond yields have recently blown out to crisis-era levels of distress, last seen at the peak of the COVID-19 turmoil:

Chinese corporate bond defaults notched a record high earlier this summer, which is now starting to impact the broader economy. The country’s latest factory activity reading revealed the first manufacturing decline since the COVID outbreak in April 2020.

Given China’s critical role as a key global growth engine, you can bet any slowdown there will ripple into European and American growth - and recent data suggests that perhaps it already has.

The bottom line: we’re seeing the early stages of a global growth slowdown, even before the coming hangover from a massive fiscal and monetary cliff. Prepare for economic and financial turbulence ahead.

Stay tuned for more updates!

Good investing,

Ross Hendricks